Home › Forums › ⚖️ CRIME INVESTIGATION LIST ⚖️ › R4bn Sanral bridge contract awarded to ‘defunct business’ with R418m debt pile

- This topic is empty.

Viewing 1 post (of 1 total)

-

AuthorPosts

-

2023-03-06 at 14:59 #396137

Nat QuinnKeymaster

Nat QuinnKeymasterState-owned roads operator Sanral in November 2022 awarded one of its largest recent contracts to a local construction firm and a Chinese conglomerate. But the winning bidders’ financials look deeply worrying, bid documents reveal.

Mecsa Construction, one of the contractors tasked with building the long-awaited Mtentu Bridge in the Eastern Cape, clinched this huge South African National Roads Agency (Sanral) tender despite a R418-million debt pile evident in the financials it submitted for the bid.

Sanral in November 2022 awarded the R4-billion Mtentu Bridge contract to a joint venture (JV) made up of Mecsa Construction — a South African firm — and China’s state-owned China Communications Construction Company (CCCC).

We would like our readers to start paying for Daily Maverick…

…but we are not going to force you to. Over 10 million users come to us each month for the news. We have not put it behind a paywall because the truth should not be a luxury.

Instead we ask our readers who can afford to contribute, even a small amount each month, to do so.

If you appreciate it and want to see us keep going then please consider contributing whatever you can.

Financial statements included in the bid documents reveal that especially Mecsa was in a dire financial position when it bagged the contract.

After reviewing the financials, one chartered accountant told us Mecsa was effectively a “defunct business”.

The company failed to submit financial statements for the period beyond the 2019 financial year, raising concerns that its current position may be even more perilous than it had been in the years under review.

Scorpio obtained the bid documents through a Promotion of Access to Information Act (PAIA) request.

The documents also raise concerns over CCCC’s finances.

The proposed Mtentu Bridge in the Eastern Cape. (Image: mecsa.net.za)

Apart from the heap of debt on Mecsa’s books, the company failed to record a profit in three of the four financial years that were reviewed for the bid. The company instead suffered losses totalling R310-million in the 2017 to 2019 period.

We put detailed queries regarding Mecsa’s finances to Charles Nonkonyana, the company’s CEO and executive chairman.

“Mecsa has no comment, sir, Sanral is best placed to answer these questions,” said Nonkonyana.

Sanral and the Development Bank of Southern Africa (DBSA), which had been roped in to oversee the bid process, said any risks associated with the contractors’ financials will be managed through strict provisions in the contract.

‘High level of risk’

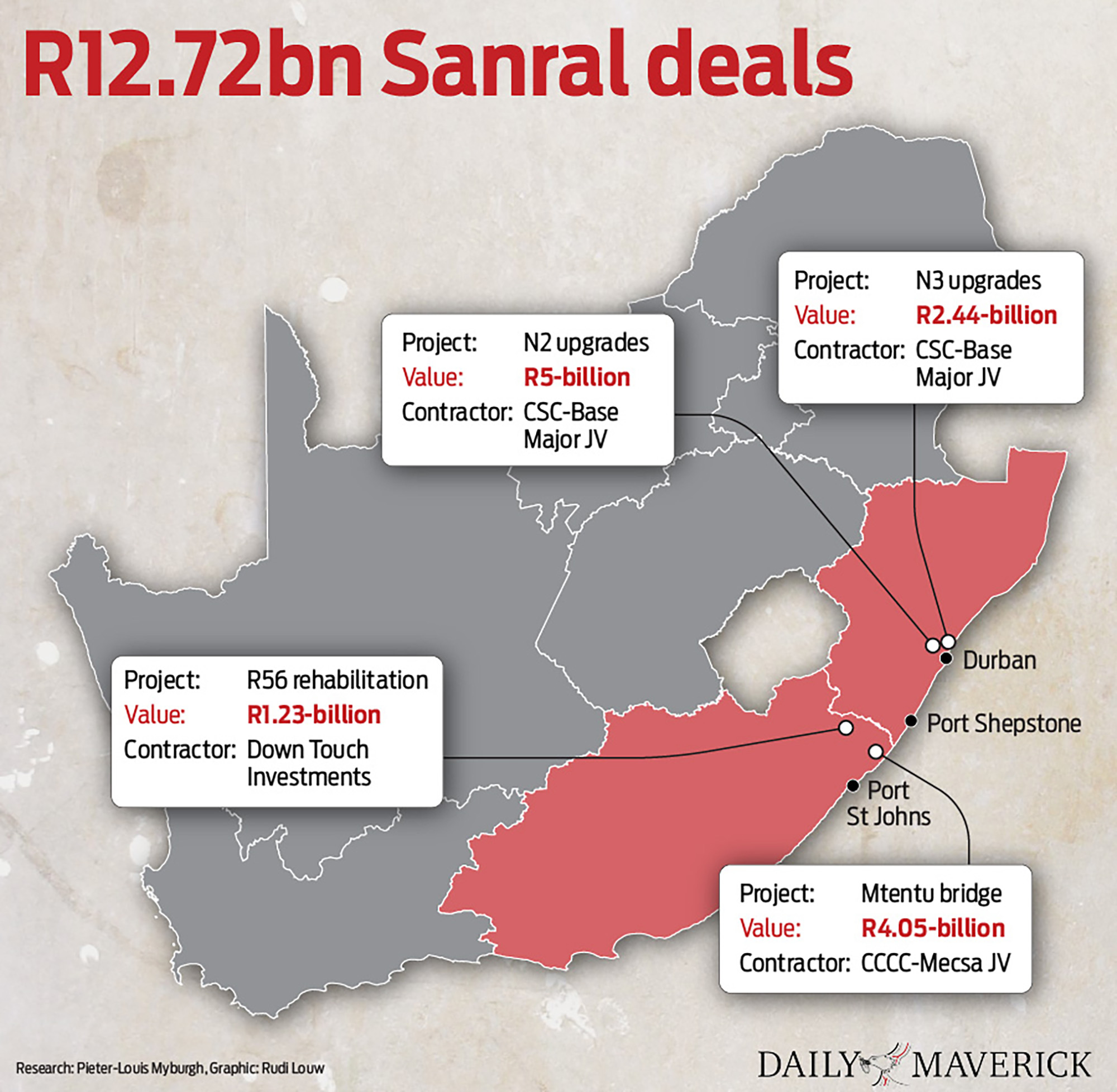

The Mtentu project is among four new contracts with a combined value of nearly R13-billion that Sanral dished out in late 2022.

The bulk of this spend will go to CCCC and its fellow Chinese state-owned entity, the China State Construction Engineering Corporation (CSC), together with their respective local JV partners.

The Mtentu Bridge forms part of Sanral’s broader N2 Wild Coast Road Project. The Mtentu bridge received special mention in President Cyril Ramaphosa’s recent State of the Nation Address.

Once completed, the bridge is set to be the tallest in Africa.

Along with Sanral’s nearby Msikaba bridge, the Mtentu project will benefit the local construction industry and boost job creation, Ramaphosa promised.

But the bid documents and the accompanying financial statements cast doubt over Mecsa’s ability to partake in the Mtentu project without running into serious financial constraints.

An analysis of Mecsa’s and CCCC’s financials by DBSA highlighted several concerns.

The DBSA acted as Sanral’s “support agency” for the 2022 contracts and assisted in evaluating the bids.

Despite worrying trends in especially Mecsa’s financials, the DBSA nevertheless recommended the CCCC-Mecsa JV for the Mtentu project.

According to a report from the DBSA’s bid evaluation committee (BEC), Mecsa only provided financial statements for the period between 2016 and 2019. “The entity did not submit any annual financial statements for 2020 and 2021, which poses a challenge in analysing the current financial position of the entity,” reads the report.

Mecsa’s older financial statements, along with the DBSA’s analyses, reflected the following:

-

Mecsa posted losses of R56-million; R124-million and R130-million respectively in the 2017, 2018 and 2019 financial years.

-

In 2019 Mecsa had total liabilities of R1.48-billion and total assets of just more than R1-billion, leaving the company with “negative equity” of R418-million. In other words, the company was neck-deep in debt.

-

The company’s current ratio, which measures its ability to pay short-term obligations, or those that are due within a year, is cause for concern. “In conclusion, the entity is not in a position to meet its current obligations,” states the DBSA report.

-

Mecsa’s operating cash flow, which measures how well a company is able to pay off current liabilities with the cash flow generated from its core business, is another red flag. “The results from the analysis reveal that the entity is not generating sufficient revenues from its core business operations,” the report determined.

-

What’s more, Mecsa had a “negative solvency position” and a “negative debt to asset ratio”.

* The DBSA report concluded that Mecsa’s financial standing “show[s] [a] high level of risk for the period under review”.

Jonathan Cruise, a chartered accountant and Daily Maverick Insider, agreed that Mecsa’s finances were in shambles, at least according to the financials it submitted for the Sanral bid.

Said Cruise: “They keep on using their creditors’ money to run a defunct business. How can they ever repay their creditors if they keep on making massive losses?”

Another charted accountant and Daily Maverick Insider agreed that Mecsa’s financial position looked bad. This person asked to remain anonymous.

“The negative gross profit margin, current ratio, solvency ratio and debt-to-asset ratio are all indicators that Mecsa is in financial distress after poor financial performance,” said the CA.

Cruise said he was even more worried over the fact that Mecsa failed to submit financial statements for the 2020 and 2021 financial years.

“The analysis [for the Sanral bid] was carried out in late 2022. By then, their latest AFS [annual financial statements] should have been ready for submission. The Companies Act compels them to have AFS for those periods.”

Cruise wonders why Mecsa omitted those documents in their bid application.

“Perhaps the auditors were not able to give them a good enough audit opinion, due to the terrible shape the company was in even before Covid,” he suggested.

Charles Nonkonyana, Mecsa’s CEO and executive chairman. (Photo: mecsa.net.za)

The DBSA told us it did request more recent financials from Mecsa.

“The CCCC-Mecsa JV formally responded with supporting documents from their accredited accounting firm, stating that the latest two years of annual financial statements for Mecsa were under auditing,” explained the DBSA.

According to the bank, Mecsa’s accountants claimed the latest financials were due to be finalised in October 2022.

We asked Mecsa’s Nonkonyana for copies of the latest financial statements, but those were not provided to us at the time of writing.

Chinese JV partner

Mecsa’s JV partner, China’s state-owned CCCC, did submit statements for the 2019, 2020 and 2021 financial years.

The statements suggest the company is in a better financial position than Mecsa, but the DBSA report raises a few issues worth mentioning.

We emailed queries to CCCC, but received no response.

Like Mecsa, CCCC did not have sufficient operating cash flow from ongoing business operations to meet its financial obligations.

“However, the entity is showing an improvement in their operating cash flow,” the report found.

Mecsa also did not have “enough liquid assets to finance their future projects”.

Concerning CCCC’s solvency ratio, the DBSA report found that the company “can be considered a higher risk entity relying an average of 2,66 times more on debt than equity” to meet its financial obligations.

CCCC also seems somewhat tardy when it comes to collecting monies from its debtors. The conglomerate is even slower in terms of paying its creditors.

According to the DBSA report, the CCCC on average waited 207 days, or roughly seven months, to get its invoices settled by debtors.

In 2021, it took the CCCC on average more than eight months to pay its suppliers. In 2020, the company waited nine months before it paid suppliers and service providers, the report reveals.

Should CCCC continue this trend, local sub-contractors and suppliers for the Mtentu project could face severe liquidity problems.

DBSA, Sanral confident in JV

We asked the DBSA why it recommended the CCCC-Mecsa JV despite what appear to be clear red flags in the two entities’ financials, especially Mecsa’s.

“Analysis of financial statements forms part of risk assessment of bidders and does not constitute a disqualifier, nor grounds to not appoint a service provider in the context of the advertised tender conditions,” stated the DBSA.

It added: “Issues of financial risk are assessed holistically and within the context of the financial position of the joint venture, and not singularly focused on only one party of the bidding joint venture.”

The DBSA also pointed us to CCCC’s track record.

“It is worth noting that according to information available in the public domain, CCCC is Africa’s largest international contractor, publicly traded, with a 40-year history of building some of the continent’s largest infrastructure projects with reported revenue of $70-billion.”

Concluded the DBSA: “The possibilities of financial problems or liquidity risks are managed through mandatory contractual requirements, including but not limited to construction guarantees and appropriate insurance.”

Sanral said it had “approved the appointment of CCCC-Mecsa based on the recommendation made by [the] DBSA after following the procurement prescripts. Sanral also based its decision on the Sanral and DBSA Internal Audit and Legal proactive assurance reports.”

Regarding the average timeframe within which CCCC paid its suppliers, Sanral stated: “Sanral has its own project management standard operating procedures, which ensures that contractors perform in accordance with the signed contract.

“Specifically, Sanral pays its suppliers and contractors within 30 days from receipt of an invoice and ensures that subcontractors are also paid within the same timelines. Any default by a contractor will be managed through contractual provisions.”

The full responses from the DBSA and Sanral are available below:

SOURCE:R4bn Sanral bridge contract awarded to ‘defunct busines… (dailymaverick.co.za)

-

-

AuthorPosts

Viewing 1 post (of 1 total)

- You must be logged in to reply to this topic.